Mauricio Junior

Mauricio Junior

What to do when I have a mortgage to pay monthly, a limited salary, and I would like to buy a condo to rent and make money?

Think about finances

You’re thinking in the right direction - but this only works if the numbers are disciplined. With a mortgage, limited salary, and a goal to buy a rental condo, the game is about ...

Subscribe easy2invest.org

Make your money work for you. Articles, videos, shorts, ebooks, books, forum, community and more.

You can cancel anytime.

Log In

Subscribe now

All information in this article is not a recommendation.

We show examples, and you need to analyze.

We are not responsible for your decisions and investments.

Related articles

Conquiste a sua aposentadoria no Brasil

Como pagar a sua aposentaria mesmo vivendo fora...

The best credit card to increase my credit score

If your goal is increasing your credit score...

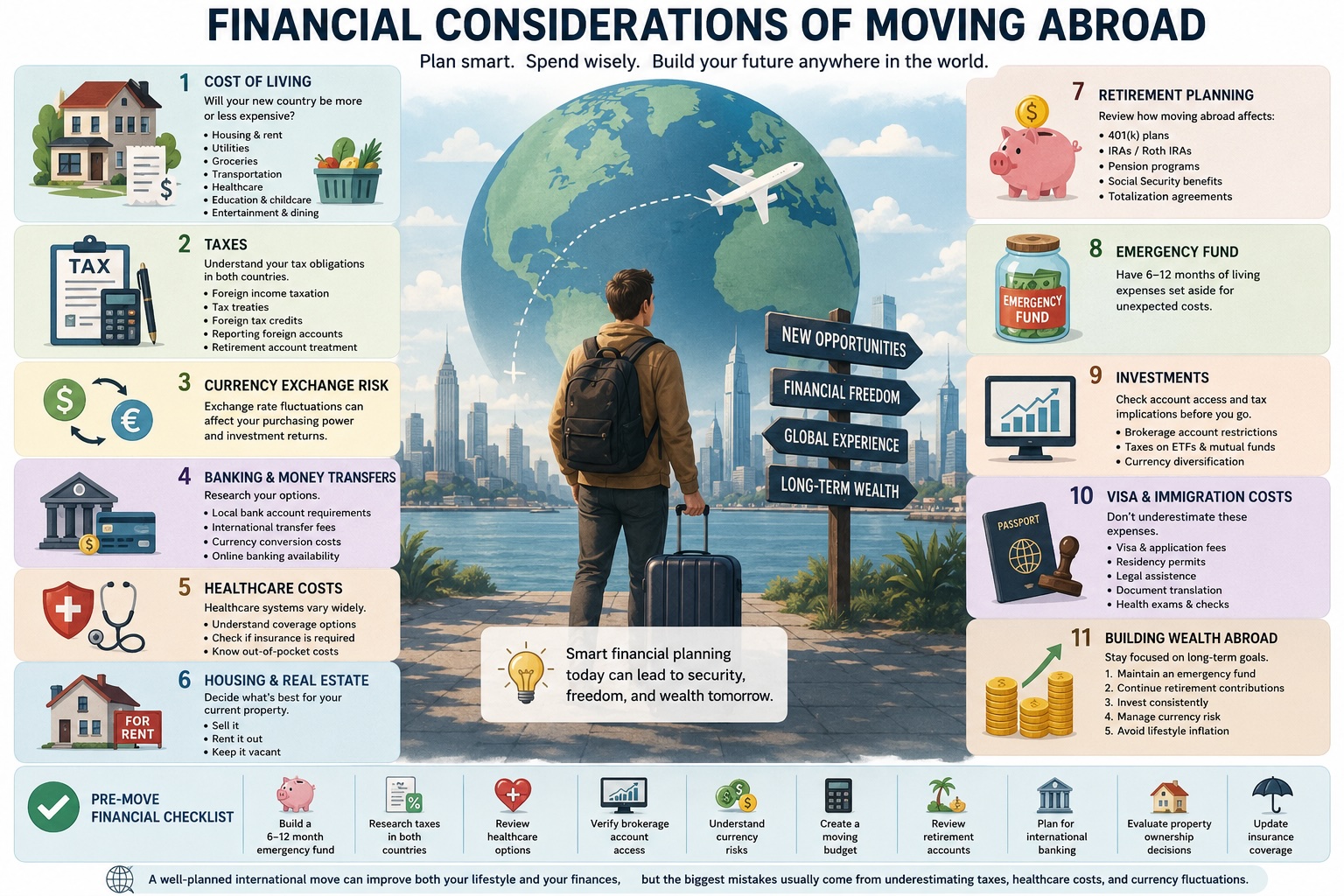

The financial considerations of moving abroad

Moving abroad can be an exciting opportunity...

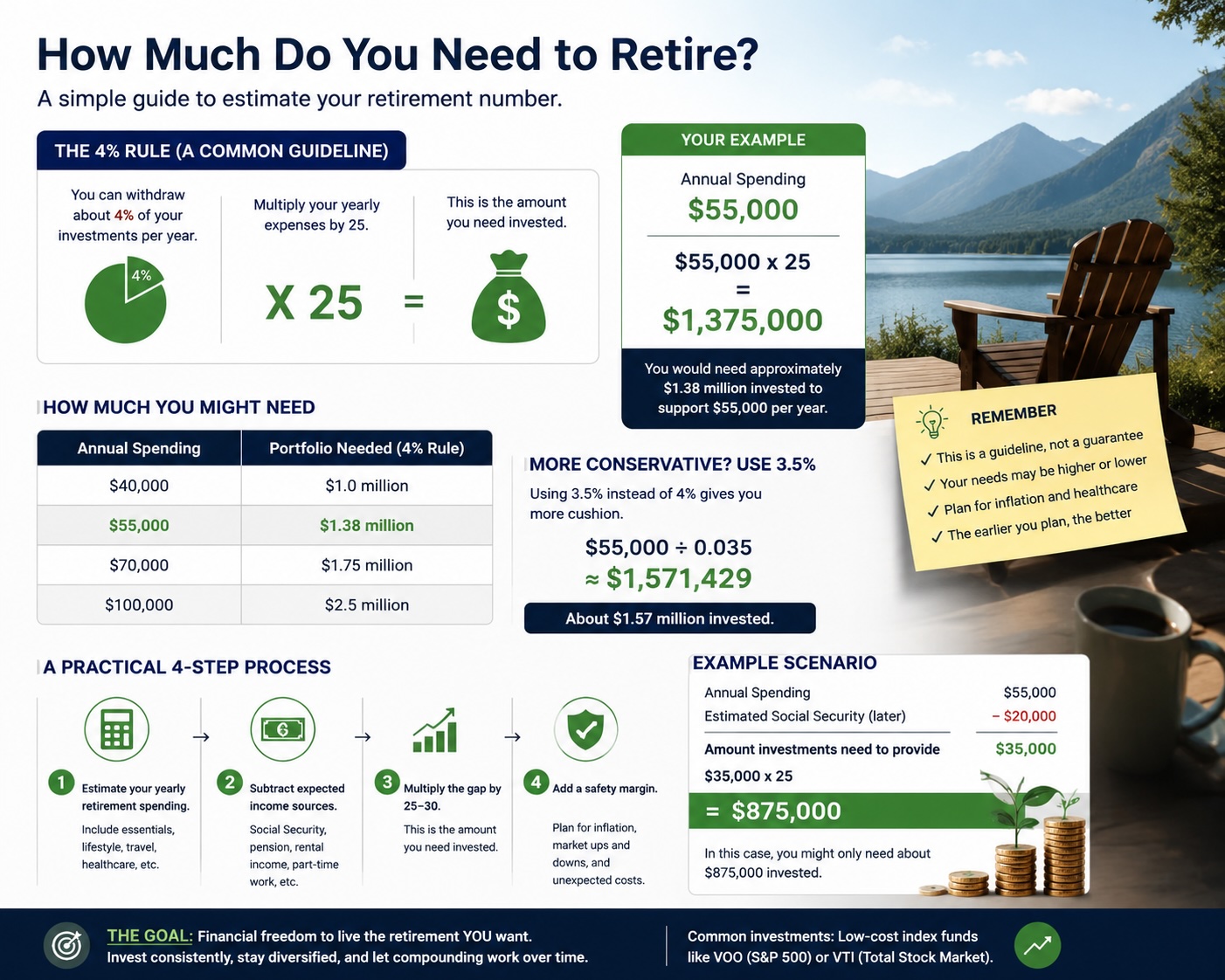

How do I figure out how much I'll need to retire?

Start with the first step, how much you...

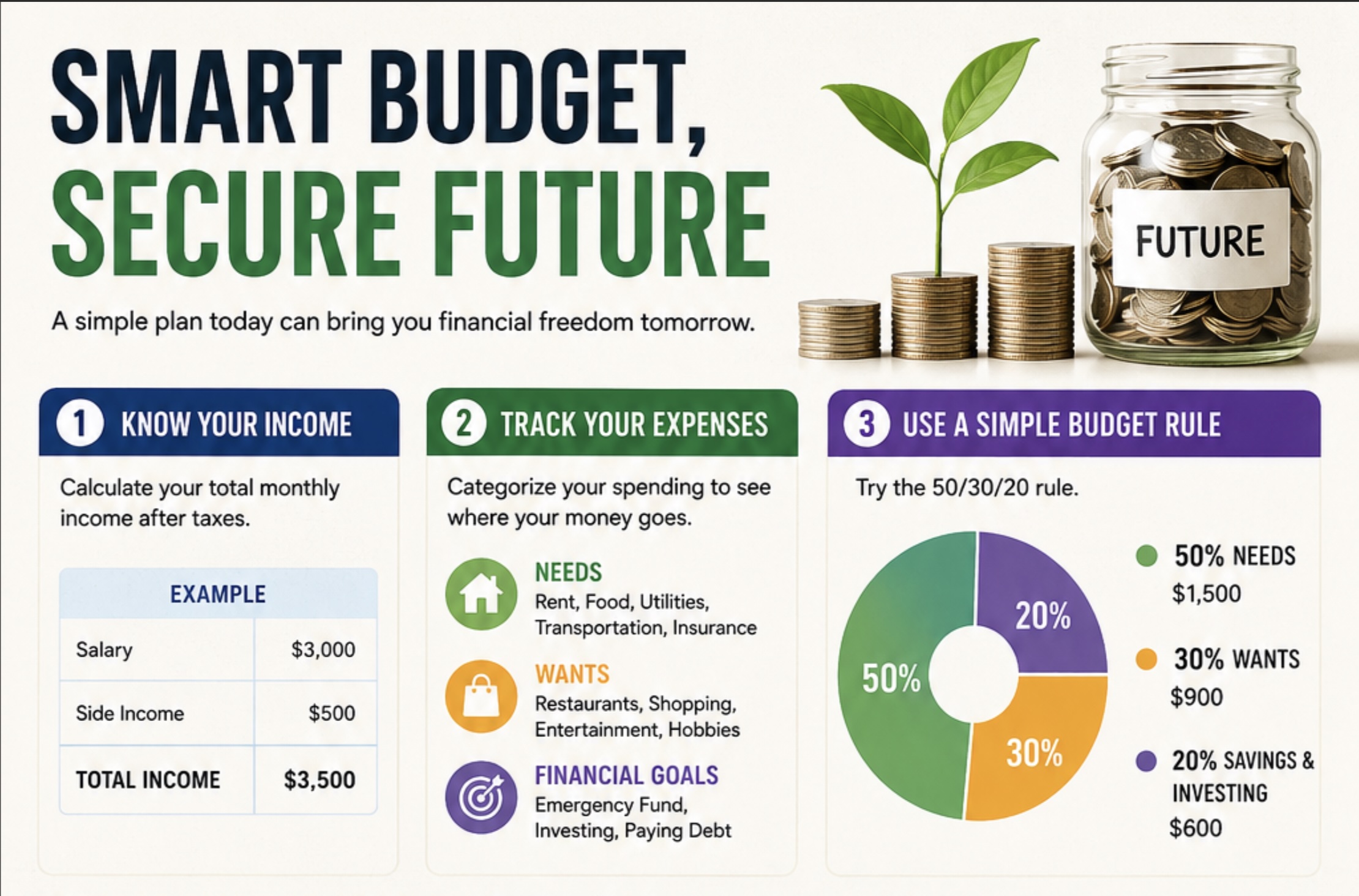

How to deal with the finance budget?

Managing your finances is about controlling ...

MSTR Bitcoin

MSTR is the stock of Strategy...

When is it a good time to buy Bitcoin?

There’s no “perfect” moment to buy Bitcoin but...

What is the best broker to use now, based on trust?

Check here the best brokers to use

Smart Budget Tracker

How to control it?

Rules about IRA Individual Retirement Account

Step by step with examples