Mauricio Junior

Mauricio Junior

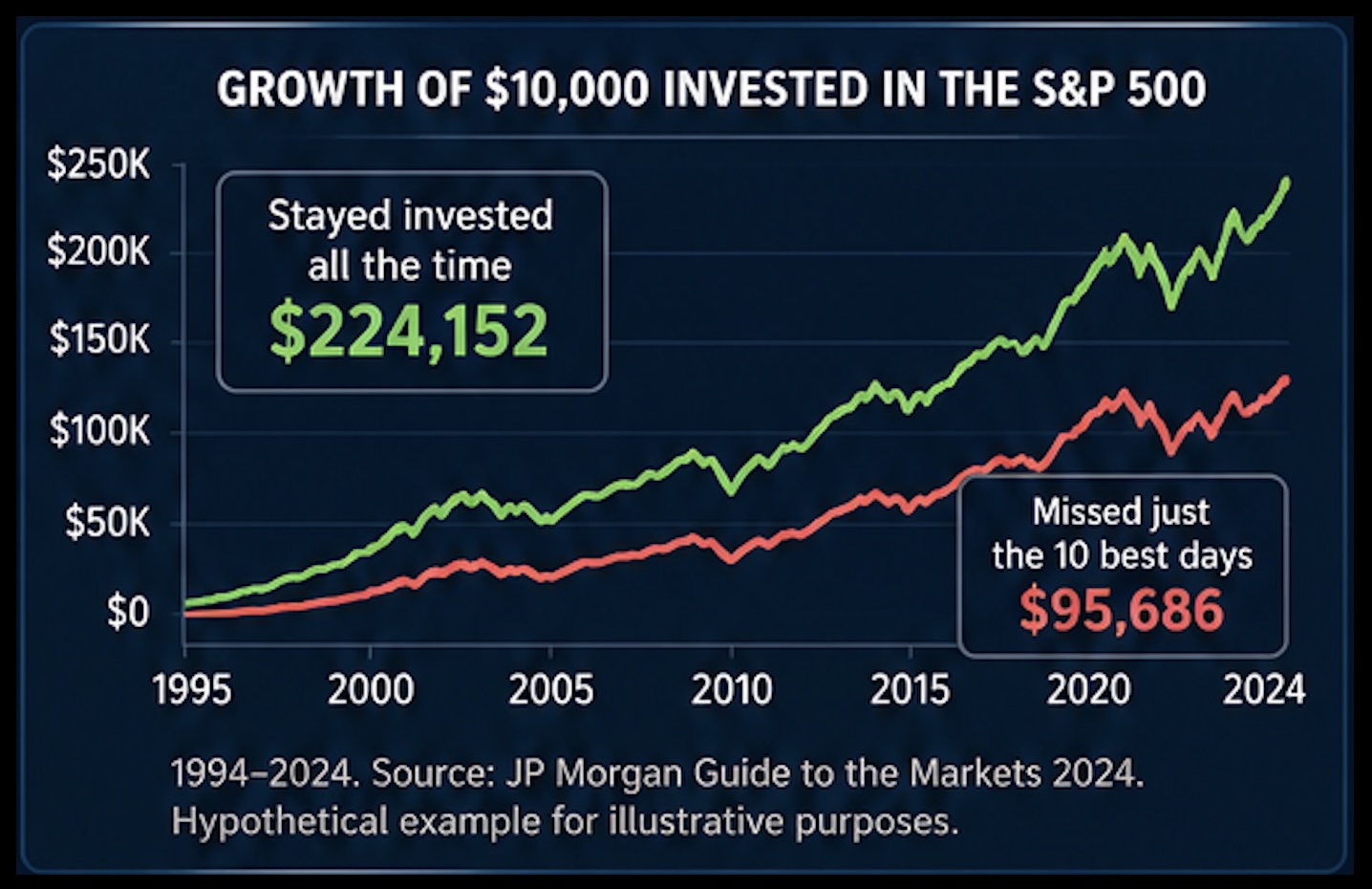

Can I move my 401k from my old company to my new 401k?

Yes — in most cases you can...

Yes — in most cases you can move your old 401(k) into your new employer’s 401(k), and this is called a 401(k) rollover.

Your main options

When you leave a job, y ...

Subscribe easy2invest.org

Make your money work for you. Articles, videos, shorts, ebooks, books, forum, community and more.

You can cancel anytime.

Log In

Subscribe now

All information in this article is not a recommendation.

We show examples, and you need to analyze.

We are not responsible for your decisions and investments.

Related articles

A good strategy to pay me first and conquer the first emergency reserve

A great way to build your emergency savings...

Invest in STRC: Is it a good idea?

Strategy's Variable Rate Series A Perpetual Stretc

The best ETFs, REITs, and BONDs

If you're building long-term wealth...

How to invest my first $2000 on stock market?

If you're investing your first $2,000, your bi...

Is the stock market made by cycles?

Yes. The stock market tends to move in cycles...

The best time or day to buy on the stock market?

There is no single best day or hour to buy stock..

Best brokers to start investing

If you're just starting to invest in the U.S. ...

Your first investment under 35 dollars for beginners

Many people believe they need thousands of d...

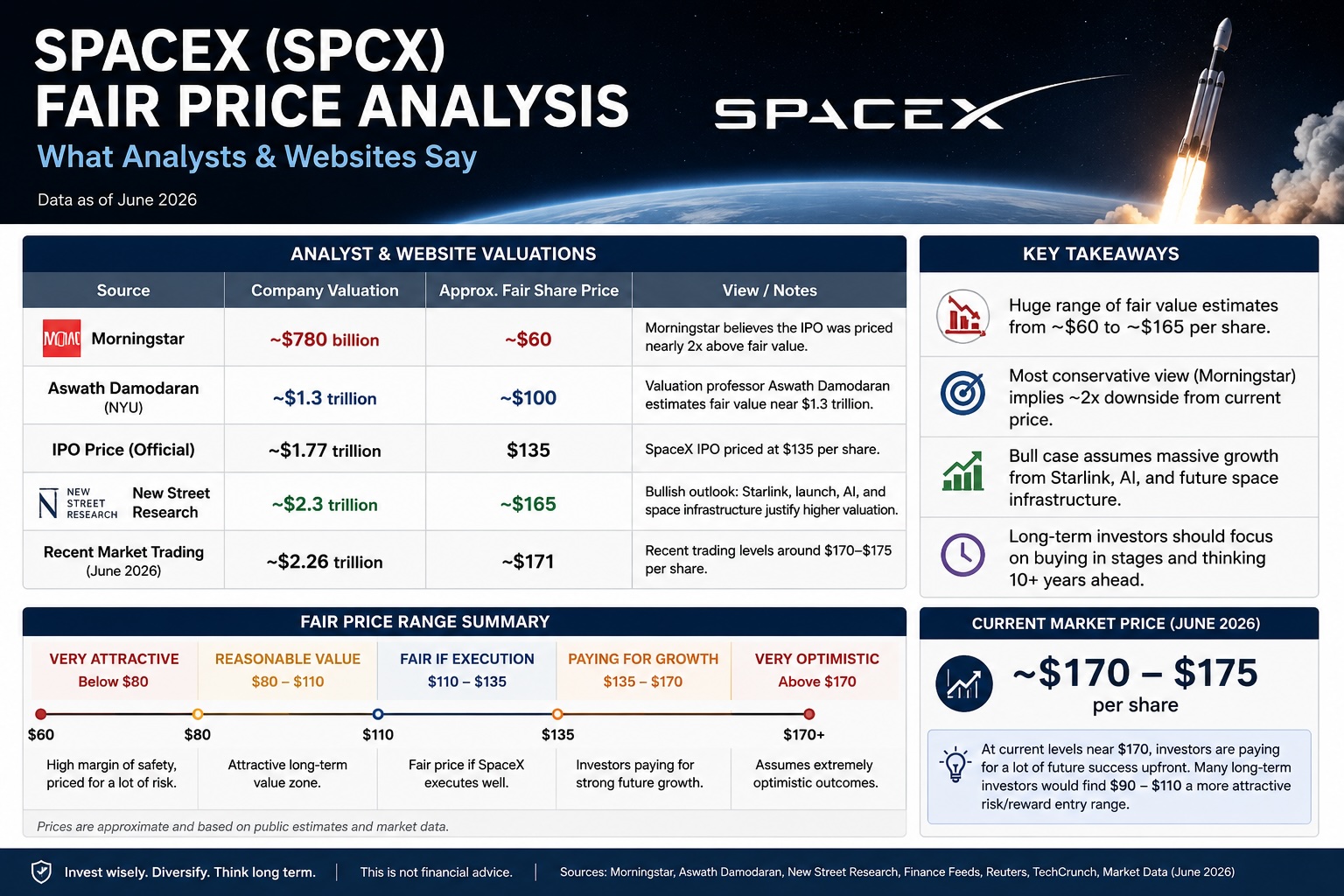

What is the fair price of SPCX (SpaceX)?

SpaceX's IPO was priced at $135 per share, and...

SpaceX will pay dividends?

As of June 2026, SpaceX has explicitly stated...